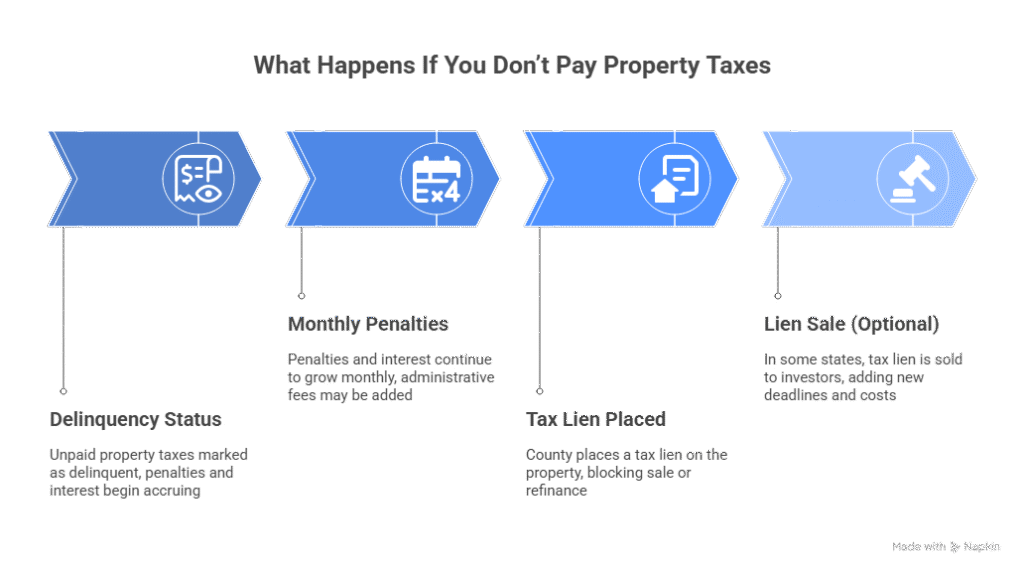

Not paying property taxes in the U.S. can lead to serious consequences sooner than many homeowners realize. When these taxes go unpaid, counties respond quickly with penalties, interest, and eventually a tax lien, an action that can turn into foreclosure if the debt continues.

Recent data published by Cotality shows that property-tax delinquencies reached 5.1% in 2025, a rise that has pushed many counties to improve penalty timelines. In this post, you’ll learn what happens if you don’t pay property taxes, how long you can delay payment, and when your home may genuinely be at risk.

Need support after a scam? Join our community today.

What Happens If You Don’t Pay Property Taxes?

When you don’t pay property taxes in the U.S., the process moves in three stages:

- Immediate penalties

- A tax lien on your home

- Possible foreclosure, if the debt continues

Counties follow this sequence because property taxes fund local services, and unpaid balances must be recovered. To make this easier to follow, here’s a quick look at the usual stages counties go through when property taxes aren’t paid:

| Stage | What It Means | Typical Consequences |

| Penalties & Interest | Account becomes delinquent | Fees added monthly |

| Tax Lien | Legal claim placed on the property | Blocks selling/refinancing |

| Foreclosure | County takes legal action | Risk of losing the property |

1. Immediate consequences: penalties, interest, and delinquency status

The first thing that happens is that your unpaid balance is marked as delinquent. From there, counties add penalties and interest that grow monthly, making the debt harder to catch up on. Some states also charge administrative fees once the account enters delinquency.

2. Medium-term consequences: the tax lien

If the taxes remain unpaid, the county places a tax lien on your property. This gives the county a legal claim over your home and blocks you from selling or refinancing until the debt is cleared. In some states, tax liens are sold to investors, which can add additional costs and deadlines.

3. Worst-case scenario: tax sale or foreclosure

If the debt continues over time, the county can move forward with a tax sale or tax foreclosure. A tax sale may involve selling the lien to a third party, who then gains the right to collect the debt or take ownership if it’s not paid. A tax foreclosure, on the other hand, allows the county to take legal possession of the property and transfer ownership to a new party.

How Long Can You Go Without Paying Property Taxes in the U.S.?

The amount of time you can go without paying property taxes varies by state, but the window is usually shorter than people expect. In many cases, counties begin adding penalties immediately, mark the account as delinquent within a few months, and may proceed to place a tax lien if the bill remains unpaid.

While every state has its own rules, the general pattern across the U.S. is similar: the longer the delay, the faster the consequences grow.

Average Timelines by State

While exact deadlines may vary, most states fall into three general timelines:

- 3–6 months: Your account is marked as delinquent, and penalties and interest begin to accumulate.

- 6–12 months: Counties typically start the tax-lien process. In some states, liens are sold to investors within this period.

- 1–3 years: This is the most common range for foreclosure eligibility. Some states move faster, while others offer longer redemption periods, but very few allow unpaid taxes to stay untouched beyond this point.

These ranges are broad, but they give you a realistic idea of how quickly a late payment can turn into a serious issue.

Have questions about dealing with scams? Contact us for support.

What Happens If You Have a Mortgage?

Whether your property taxes are handled through escrow or paid directly by you affects how the entire process develops. The county follows the same rules either way, but your lender’s involvement can change the timeline, the fees, and even the risks you might face.

Here is how each situation typically works:

1. When Your Lender Pays Your Taxes Through Escrow

If your mortgage includes an escrow account, your lender is responsible for paying your property taxes on time. Issues begin only when the escrow balance falls short.

What Usually Happens?

- The lender pays the shortage, so the taxes stay current

- Your monthly mortgage payment increases to recover the difference

- You avoid penalties and delinquency, but your housing costs rise

📌Escrow protects you from missing payments, but shortages can still impact your budget.

2. When You Don’t Have Escrow, You Are Fully Responsible

If you pay your property taxes directly and miss a payment, the county marks the account as delinquent and follows its standard collection procedures. Lenders track this closely, and many take action to protect their interest in the property.

What Lenders May Do Next?

- Open a forced escrow account

- Add new charges to your monthly payment

- Make the forced escrow permanent for the rest of the loan

📌Forced escrow is common when taxes are unpaid because it suggests the lender can cover future bills.

3. How Your Lender Reacts If the Tax Debt Keeps Growing

When the delinquency becomes serious, the lender may decide to pay the taxes directly. This prevents the county from moving forward with actions that could put the property at risk.

If the lender pays the taxes for you:

- The amount is added to your mortgage balance.

- Your monthly payment increases.

- Additional fees may be included.

- Missing future mortgage payments becomes more likely.

📌This step often hints that the situation needs immediate attention before it becomes harder to recover from.

How To Avoid Losing Your Home Over Property Taxes

If you’re behind on your property taxes, don’t panic because most states offer programs that can help you catch up and make the debt more manageable. They might reduce what you owe, break it into payments, or lower your future bills.

Here are the most practical steps you can take:

1. Set Up a Payment Plan With Your County

Many counties allow you to pay your overdue taxes in installments. This can be helpful if the balance is high or if penalties have grown over time. You can get:

- A structured monthly payment plan.

- A clear deadline to pay the full amount.

- Possible reduction in penalties once you enroll.

2. Apply for Homestead Exemptions

If the property is your primary residence, you may qualify for a homestead exemption. This reduces your taxable value, which can lower future tax bills. This may help you:

- Reduce your annual property tax amount.

- Prevent new delinquencies.

- Stabilize your budget for the long term.

3. Look Into Programs for Seniors, Veterans, and People with Disabilities

Many states offer additional tax relief for specific groups. If you qualify, these programs can make a long-term difference in keeping your home secure. Some common benefits include:

- Lower tax rates.

- Frozen tax assessments.

- Partial or full exemptions.

4. Talk to a Local Tax Professional

If the debt is growing fast, or you’ve received several warnings, it’s a smart move to speak with a tax expert. They can explain your rights, help you deal with the county, and verify that all fees are accurate. A professional is especially helpful when:

- You are already in the lien stage.

- Your lender has added charges to your mortgage

- You need to verify the county’s timeline or fees.

Protecting Your Home Starts With Small Steps

Property taxes aren’t just another bill: they’re part of how every community keeps basic services running. When something interrupts your ability to pay, the situation can feel heavy, but it doesn’t define your future. Counties expect communication, not perfection, and most are willing to work with you when you reach out early.

If you’re dealing with a balance that feels out of reach, small steps still move you forward. Asking questions, reviewing deadlines, or requesting a payment option can ease the pressure and help you maintain control. You deserve clear guidance and a real path to relief.

We Want to Hear From You!

Fraud recovery is hard, but you don’t have to do it alone. Our community is here to help you share, learn, and protect yourself from future fraud.

Why Join Us?

- Community support: Share your experiences with people who understand.

- Useful resources: Learn from our tools and guides to prevent fraud.

- Safe space: A welcoming place to share your story and receive support.

Find the help you need. Join our Facebook group or contact us directly.

Be a part of the change. Your story matters.

Frequently Asked Questions (FAQs) About What Happens If You Don’t Pay Property Taxes

What Happens if You Don’t Pay Property Tax?

If you don’t pay property taxes, the county adds penalties, marks your account as delinquent, and can place a tax lien on your property. If the balance is unpaid, the process may move toward a tax sale or foreclosure, depending on your state.

What Happens if You Ignore the Notices?

Ignoring notices does not slow down the process. The county continues with its legal timeline, which may lead to:

- Penalties and additional fees.

- A tax lien is placed on your property.

- The lien is being sold to an investor in some states.

- The process is moving closer to foreclosure.

Who Should You Contact First if You Fall Behind?

The best place to start is your county tax office. They can walk you through your current balance, deadlines, payment plan options, and any fees that may already apply. If the notices are starting to pile up or things feel confusing, talking to a local tax professional can help you understand your options and figure out your next step.

Photos via Freepik.