In 2025, tax agencies finally integrated cryptocurrencies into mainstream regulatory compliance. New reporting forms, such as the U.S. 1099-DA, stricter KYC regulations, and smarter blockchain analytics have turned so-called private wallets into open books.

Investors who once depended on anonymity now face audits, back taxes, and, in some cases, jail time. In many countries, cryptoassets tax evasion convictions are piling up. In this post, you’ll learn how authorities are tracking offenders, real tax evasion cases from the U.S. and beyond, and what you need to know to stay on top of the law.

Need support after a scam? Join our community today.

What Is Crypto Tax Evasion?

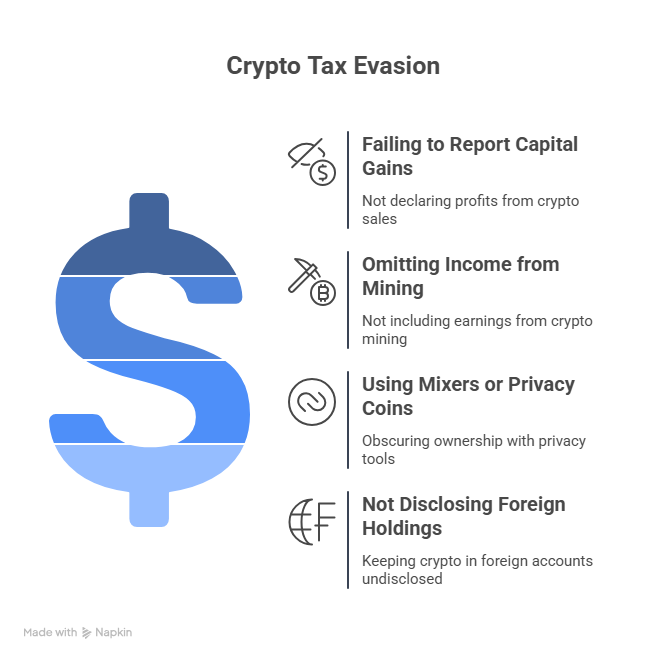

Tax evasion using crypto assets is when people or entities deliberately underreport, misreport, or hide income earned from digital currencies like Bitcoin, Ethereum, or stablecoins. This is not about forgetting to file a form; it is about intentionally avoiding obligations. Some common forms of crypto tax evasion include:

- Failing to report capital gains from selling or trading crypto.

- Omitting income from mining, staking, or airdrops.

- Using mixers or privacy coins to cover up ownership.

- Not disclosing crypto held in foreign exchanges or wallets.

💡It’s important to separate tax evasion from tax avoidance, which is a legal and honest mistake. Intent is what divides a criminal act from an error. If the omission is intentional and meant to deceive, it counts as evasion, and that’s when legal actions begin.

How Tax Authorities Track Crypto Transactions?

Tax authorities around the world are no longer in the dark when it comes to digital assets. Thanks to modern tools and legal mechanisms, they’re getting better at connecting transactions to real identities. Here’s how they’re doing it:

1. Forensic analysis and collaboration with specialized firms

Contrary to popular belief, most cryptocurrency transactions are not anonymous. They’re recorded on public ledgers that anyone, including tax authorities, can analyze. Agencies now use advanced blockchain forensics tools like Chainalysis or TRM Labs to trace movements across wallets, identify patterns, and match them to real identities.

2. The 1099 Forms and Exchange Reporting

In the U.S., exchanges like Coinbase, Kraken, and Gemini are now required to issue Form 1099-DA (as of 2025) to report user activity directly to the IRS. These forms include data on gains, losses, and even wallet movements, giving the IRS a detailed view of a taxpayer’s crypto behavior.

3. John Doe Summons: Catching the Unknowns

When investigators suspect underreporting but don’t have names, they can issue a John Doe summons. This legal tool forces exchanges to hand over customer data for a whole group of users. That’s how they built the case against Ahlgren, and how they’re building more every year.

4. Data‑matching and pattern detection

Tax agencies cross-reference blockchain data with self-reported income and third-party sources like bank records, platform payouts, and online wallets. This helps uncover inconsistencies or hidden activity, providing leads for new fraud investigations.

Which Actions Raise Warning Signs for Tax Authorities?

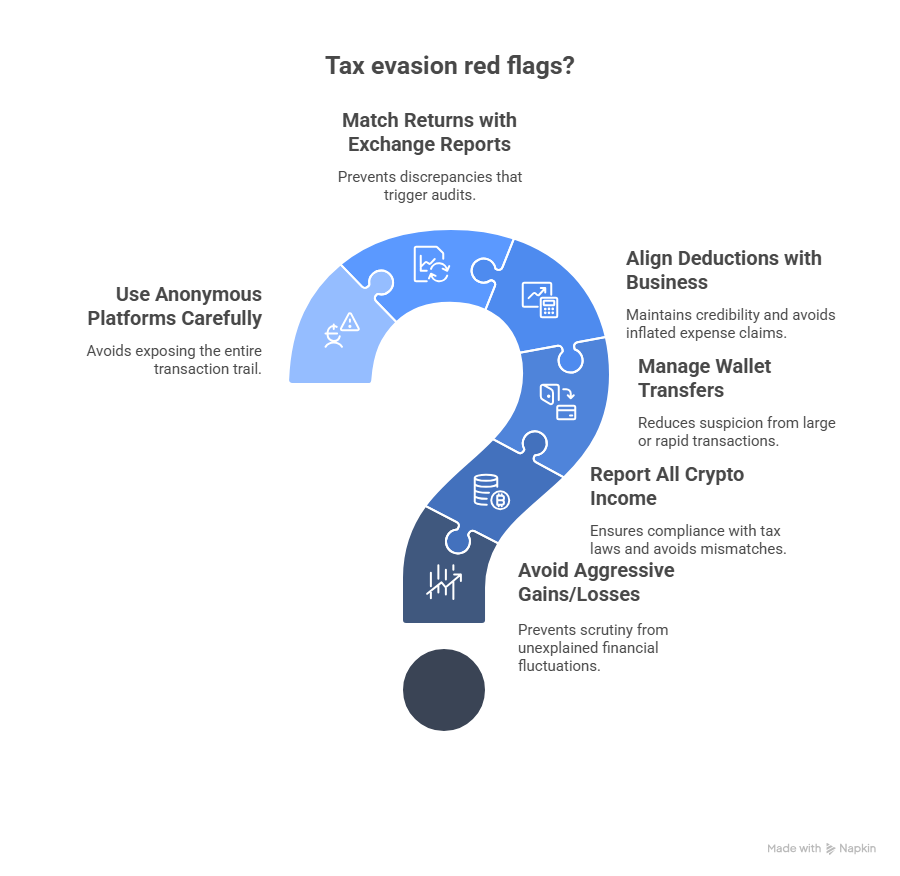

Certain behaviors consistently appear in crypto tax evasion cases. These are the patterns tax agencies monitor when deciding who to investigate or prosecute:

- Aggressive Gains or Losses Without Explanation: Submitting returns with steep crypto gains or notable losses year after year can raise scrutiny. The IRS may view this as manipulation or improper reporting, especially if there’s no supporting documentation.

- Missing Income from Trades, Airdrops, or Staking: Crypto-to-crypto trades, airdrops, forks, and staking rewards are all taxable. If a taxpayer only reports fiat conversions or omits digital activity entirely, it often results in mismatches with the 1099 forms that exchanges send to the IRS.

- Rapid or High-Value Transfers Between Wallets: Large or fast-moving transfers between wallets, especially when followed by fiat withdrawals or luxury purchases, raise questions. These flows are traceable, even across privacy layers.

- Deductions That Don’t Fit With Real Crypto Business: Large home-office deductions or business write-offs tied to crypto must match actual operations. Self-employed traders or advisors often draw attention if their expenses seem inflated or undocumented.

- Conflicts Between Returns and Exchange Reports: When tax filings don’t match 1099-DA reports issued by platforms like Coinbase or Kraken, the IRS is automatically notified. Even small anomalies in cost basis calculations, if repeated, can lead to automated audit systems.

- Use of Anonymous Platforms or Privacy Coins: Using decentralized exchanges, mixers, or privacy coins isn’t illegal, but when those assets are later moved to KYC-compliant platforms, gaps in reporting can expose the entire trail.

Have questions about dealing with scams? Contact us for support.

United States: The First Stand-Alone Crypto Tax Evasion Conviction

In December 2024, the U.S. Department of Justice secured the first stand-alone conviction for crypto-related tax evasion. The defendant, Frank Richard Ahlgren III, was charged with knowingly failing to report over $3.7 million in Bitcoin gains earned between 2017 and 2019.

Authorities discovered that Ahlgren used different tactics to hide his profits:

- Converted large amounts of BTC into physical gold.

- Used privacy mixers to mask transaction origins.

- Made in-person cash trades to avoid leaving a bank trail.

How the IRS Caught Him?

Despite those efforts, the IRS connected the dots using:

- Coinbase 1099-K reports, which list his crypto sales.

- Wire transfer records showing fiat conversions.

- Blockchain analysis tools like Chainalysis to trace transactions.

- KYC records linking wallet addresses to his real identity.

Ahlgren was finally sentenced to two years in federal prison and ordered to pay over $1.1 million in restitution. The message was clear: even without traditional financial intermediaries, crypto transactions leave a trail, and the IRS is following it.

Cryptoassets Tax Evasion Conviction: Real Cases Around the World

Tax enforcement on crypto isn’t limited to the U.S. Tax authorities in other countries are already prosecuting crypto-related offenses. These cases are backed by official enforcement actions and show how agencies detect and punish tax evasion or illegal activity focused on digital assets:

1. United Kingdom: Cash, Crypto, and Unregistered ATMs

- Offense: Operating 11–28 illegal crypto ATMs between December 2021 and March 2022, processing over £2.5 million in transactions.

- The Punishment: Olumide Osunkoya, 46, pleaded guilty in September 2024 and was sentenced to 4 years in prison in February 2025. Charges included operating unauthorized crypto infrastructure, document fraud, and possession of criminal property.

- Enforcement: The FCA and police dismantled over 30 unregistered machines in 2023 and pursued confiscation under the Proceeds of Crime Act 2002.

2. South Korea: A Politician’s Hidden Wallets

- Offense: Kim Nam-guk, a former lawmaker, failed to declare approximately 9.9 billion won (~USD 6.8 million) worth of cryptocurrency in his 2021 and 2022 financial disclosures. Prosecutors say he converted the crypto to bank deposits and transferred funds to hide assets.

- The Punishment: Prosecutors requested a 6-month prison sentence. In October 2024, the court sentenced Kim to six months in jail for hiding assets.

- Enforcement: Charges included false asset declarations and evasion of ethics oversight.

3. Australia: Payroll Fraud Using Crypto

- Offense: Labor‑hire syndicate paid workers in crypto to evade nearly AUD 10 million in PAYG tax obligations.

- The Punishment: In December 2024, six people were convicted and sentenced to a total of 43 years in prison for non-payment of payroll tax and money laundering.

- Enforcement: Case led by a Serious Financial Crime Taskforce involving the AFP, ATO, and ASIC.

How to Stay on the Right Side of Crypto Tax Law?

Most cryptoassets tax evasion convictions start with simple mistakes: incomplete records, misreported income, or a failure to follow basic reporting rules. Preventing legal exposure requires clear habits and proper tools throughout the year.

- Track all activity: Record every trade, swap, staking reward, airdrop, NFT transaction, and crypto payment. Use tools that gather data from multiple wallets and exchanges.

- Evaluate your exchange security: Not all platforms protect customer data and assets equally. Review the security of your centralized exchanges to understand potential risks when using custodial services.

- Match your return to exchange data: Check your tax filings to align with third-party reports like Form 1099-DA or 1099-B. Discrepancies often cause audits.

- Use crypto-specific tax software: Generic tax tools often mishandle DeFi transactions, asset transfers, or cost basis calculations. Choose tools built for blockchain complexity.

- Protect access to your wallets: Losing access to private keys or wallet records can block you from proving cost basis or asset ownership. Keep your crypto wallet safe with proper backups and secure storage.

- File on time, even if you can’t pay: Late filings typically carry harsher penalties than unpaid taxes. If you can’t pay in full, submit your return anyway and apply for an IRS payment plan to stay compliant.

Crypto Tax Enforcement Is Now Unavoidable

Crypto tax enforcement is escalating fast, with agencies using advanced tools and international coordination to pursue evasion. Tax agencies have moved from reacting to crypto tax evasion to proactively hunting it, with advanced analytics, cross-border collaboration, and a growing list of convictions.

At Cryptoscam Defense Network, we help users stay ahead of this shift. As a trusted resource in crypto fraud detection, our mission is to equip you with the tools to protect your investments and recognize future risks.

We Want to Hear From You!

Fraud recovery is hard, but you don’t have to do it alone. Our community is here to help you share, learn, and protect yourself from future fraud.

Why Join Us?

- Community support: Share your experiences with people who understand.

- Useful resources: Learn from our tools and guides to prevent fraud.

- Safe space: A welcoming place to share your story and receive support.

Find the help you need. Join our Facebook group or contact us directly.

Be a part of the change. Your story matters.

Frequently Asked Questions (FAQs) About Cryptoassets Tax Evasion Conviction

Can I Go To Jail For Not Reporting Crypto Income?

Yes. In the U.S., failing to report crypto gains or income can lead to criminal charges under the Internal Revenue Code. Penalties include up to 5 years in prison, heavy fines, and restitution. Similar penalties exist in the U.K., Australia, and other jurisdictions.

What Common Tactics Do Tax Evaders Use?

Tax evaders often rely on the following strategies to hide their cryptocurrency activity from tax authorities:

- Failing to report crypto income: Simply omitting digital asset earnings from tax returns.

- Using offshore exchanges: Moving assets to foreign platforms to avoid domestic reporting requirements.

- Hiding transactions through privacy coins or mixers: Attempting to obscure transaction trails using anonymizing technologies.

- Underreporting capital gains: Declaring only a portion of profits, although modern blockchain tracking tools increasingly expose such discrepancies.

How Can Governments Improve Enforcement?

Governments can strengthen enforcement by:

- Modernize tax systems to effectively address the unique characteristics of digital assets.

- Establish clear classifications for cryptocurrencies to ensure consistent tax treatment.

- Adopt advanced technologies capable of tracing and anonymizing blockchain transactions.

- Regulate centralized intermediaries (e.g., exchanges and wallet providers) to enforce KYC and reporting obligations.

- Improve international cooperation to track cross-border crypto activities and ensure global tax compliance.

Photos via Freepik.